If you’re planning to sell your home, take note that buyers aren’t the only ones who have to pay closing costs. Sellers also need to shoulder a variety of closing costs, and it’s something you need to factor into the sale price since most of it will be deducted from the profit on your home.

While closing costs for sellers can differ due to variations in local tax laws and other requirements, you can expect to pay anywhere from 8% to 10% of the home’s sale price during closing, according to Zillow.com. It’s important that you know about these potential costs to understand your obligations as a seller and avoid unwanted surprises at closing.

Here are some of the most common closing costs for sellers:

One of the most significant closing costs you have to cover when you sell your home is the real estate agent commissions. A typical commission is usually between 4 and 6% of the sales price of the home, which will be split between the listing agent and the buyer’s agent.

The real estate commission is usually the biggest fee a seller pays, but there’s a higher risk if you choose not to hire an agent and choose to For Sale by Owner (FSBO). Since selling a home is a complicated process, it’s better to have a professional by your side who will guide you through every step and make sure you get the most profit from the sale of your biggest investment.

Commissions on real estate vary by market, and could be negotiable as long as you make a deal with your listing agent right from the start.

Another fee to keep in mind when you sell your home is title insurance fees. Sellers typically pay the buyer’s title insurance premium as part of closing costs, and the fee often varies from state to state and also based on the sales price of the home.

Title insurance protects the new owner and lender in case there are issues with your home’s title. In case there’s someone else who can claim ownership over the property, either because of a dispute over the property or because of outstanding liens from contractors, creditors, or the government, this one-time payment protects the buyer from the financial burden of sorting out title issues in court, whether they arise at closing or later down the road.

A transfer tax, also called a title fee or government transfer tax, is the tax amount that you will pay when the title for the home transfers from you to the buyer at the time of closing. It is one of the most significant fees in transferring property. The tax amount is determined by state laws, which means the cost varies a lot. This fee is also one of the main reasons why it’s difficult to get an accurate estimate of closing costs, so it might be helpful to research about it before you close the sale.

In some states, it is required by state law to have a real estate attorney oversee the closing and settlement of the real estate sale. If you have your own attorney representing you when your home is sold, you will have to consider attorney fees as part of closing costs.

Even if you are not required to hire an attorney in the state where your home is, you may want to do so especially if you are dealing with complex transactions involving distressed properties or inherited real estate.

An escrow account is held by a third party provider that protects both the buyer and seller by keeping either party from escaping with the other’s money. You can also think of escrow like a savings account that keeps the earnest money deposit safe. Escrow fees include the signing and recording of the closing documents and the deed, and the holding of all the purchase funds. You may also have to pay fees for transferring funds, copying of documents, and notary charges.

Escrow costs are usually between $500 and $2,000, or about 1 to 2% of the home sale price. The fees for escrow are usually split 50-50 between you and the buyer.

Owning a property means you have to pay property taxes, which vary widely state to state. Property taxes are usually paid in advance out of an escrow account associated with your mortgage.

When you sell your home, you’ll be responsible for prorated property taxes that have accrued up to the closing date, at which point the buyer or the new owner will take over. Be prepared as you may have to pay property taxes at closing to bring yourself up to date.

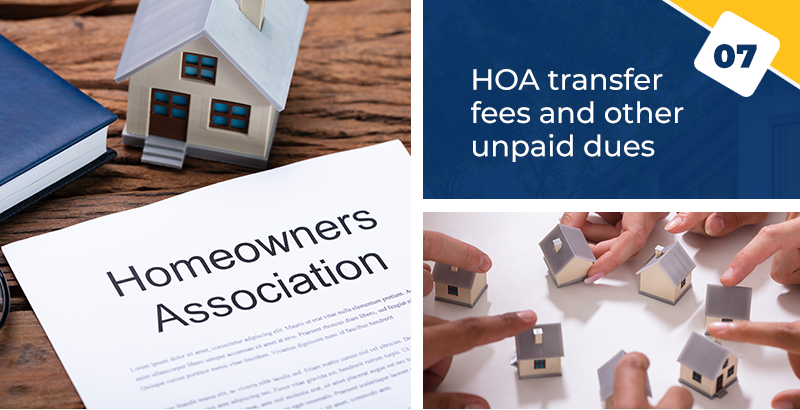

If you’re living in a neighborhood that is governed by a homeowners association (HOA), there may be HOA transfer fees to pay on top of all other closing costs mentioned above. These are standard fees that may occur when a property is transferred from one owner to another. Transfer fees are meant to cover the costs associated with preparing documents, handing out HOA’s rules to the new owner, dealing with property inspection records, changing names in the homeowner databases, changing security codes, creating new security cards, and other administrative costs.

Aside from transfer fees, you might also need to shell out some cash at closing to make sure you’ve paid up to the close date, just like with property taxes.